The world of finance doesn’t stand still. And neither does technology. Every few months, new tools reshape how we move, borrow, and invest money. From AI-driven insights to digital currencies, today’s fintech trends are transforming not just banks and startups, but the way ordinary people interact with money.

In this guide, you’ll see what’s next for 2026. We’ll look at how AI, blockchain, and embedded finance are redefining the future of financial services, and what that means for businesses, creators, and consumers around the world.

Artificial intelligence and machine learning are two emerging technologies that are changing how the financial sector operates. These technologies no longer sit in labs or pilot programs. They’re now part of how banks, insurers, and fintech companies make decisions, detect fraud, and deliver personal experiences every day.

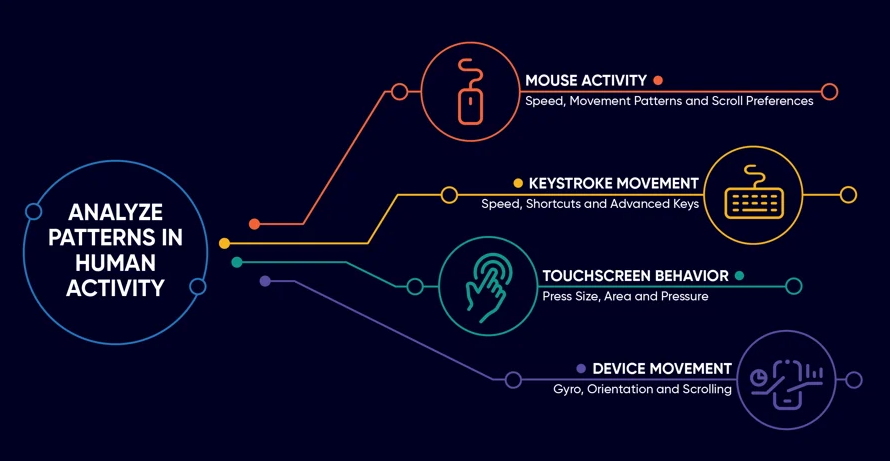

AI tools can study massive amounts of data in seconds. They learn from spending patterns, customer interactions, and typing speed. This helps financial institutions spot unusual activity before it becomes a threat. It also lets them anticipate customer needs, from predicting cash flow to offering savings advice.

A 2024 survey by BioCatch found that nearly 73% of financial institutions are already using AI to detect fraud. Yet 69% admit that criminals are currently more skilled at using AI for financial crime than banks are at using it to fight back. The finding underscores the urgency for financial firms to enhance their defences and invest in smarter, faster detection technologies.

Behavioral biometrics and liveness detection systems are great examples. BioCatch and HyperVerge use cues like typing speed and phone grip to verify identity. These provide an extra layer of protection against fraud while keeping the process simple for users.

Imagine logging into your bank account. Behind the scenes, an AI model compares your behavior to your past activity. If something feels off, like you’re typing slower or from a new location, it flags the session for review. This means faster detection and fewer false alarms for both the bank and the user.

Large language models help fintech companies study transaction history and customer preferences. They create personalized insights, like when to move funds into savings or which card offers the best rewards. The result is a smoother customer experience and stronger loyalty.

AI is also changing how people invest. Many platforms now use automated investing tools to build and manage portfolios with real-time data. They make investing easier for beginners and more efficient for experienced users. This shows how deeply AI is shaping the future of personal finance.

As AI becomes standard in fintech, it’s reshaping everything from customer onboarding to risk management. Companies that adopt these tools early gain speed, security, and trust. These are all key drivers of success in today’s market.

A major wave of fintech trends revolves around blockchain technology, decentralized finance (DeFi), and tokenization. These tools are changing how money and assets move around the world.

With smart contracts and distributed ledger technology, people can trade parts of assets instead of full ones. That means markets run faster and more efficiently. It also opens doors for investors who were once shut out.

The world of passive real estate investing also has an important role here. Instead of buying a full property, you can own small digital tokens linked to it. Each token can earn income or grow in value, giving investors flexibility and easier access to real estate opportunities.

Here are examples.

Imagine a real estate fund that uses blockchain to issue digital tokens. A small investor can buy a fraction of a commercial building through these tokens and earn passive income as rent payments are distributed automatically via smart contracts. This lowers entry barriers and supports financial inclusion, allowing anyone to participate in property investment.

DeFi platforms make lending and borrowing faster and more transparent. Instead of going through banks, users can connect wallets and transact directly with others through decentralized protocols. Smart contracts, secure funds, and interest rates are set algorithmically.

However, there are regulatory hurdles. The regulatory perception of DeFi continues to evolve as governments work to balance innovation and consumer protection. Companies that explore compliant ways to integrate blockchain‑based systems now could gain a strong advantage in the next phase of digital finance.

Another major fintech trend is embedded finance. This involves bringing financial services directly into non-financial platforms so users can pay, borrow, or invest without leaving the app.

Think about digital wallets and e-commerce platforms. They now include payment processing, Account-to-Account (A2A) transactions, and lending features that run quietly in the background. Banking is becoming invisible, as it operates wherever people already spend time online.

Here’s how embedded lending works in e-commerce.

When someone adds an item to their shopping cart, they get an instant Buy Now, Pay Later (BNPL) option. They can use and service they’d like, such as Affirm, Afterpay, or Zip. The company receives the payment in full, but the customer pays in small installments.

There’s no paperwork involved. This short-term loan takes place within seconds, built right into the checkout page. According to Stripe, businesses offering BNPL on eligible transactions have seen revenue grow by as much as 14%, showing how powerful embedded lending can be for conversions.

This is another example.

A Neobank app, like Revolut and N26, gives users spending insights, savings tools, and access to small loans, all in one place. Behind the scenes, orchestration platforms connect these services, keeping everything smooth and seamless.

Open banking and APIs (Application Programming Interfaces) are a growing fintech trend that gives customers more control, better insights, and faster access to services.

Banks, Neobanks, and tech platforms use APIs to share data securely. This lets people view all their accounts, savings, and loans in one place. It also prioritizes mobile-first banking and uses tools that help users make smarter financial decisions.

Let’s look at an example of open banking in action.

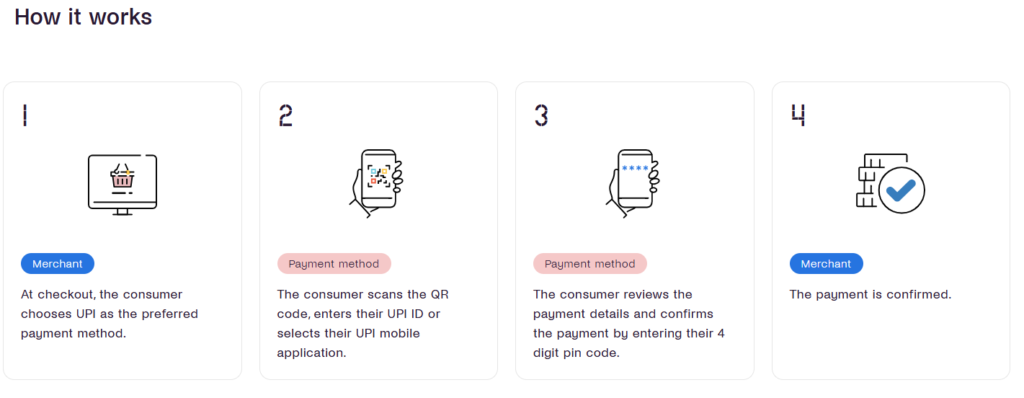

India’s Unified Payments Interface (UPI) shows how open banking can work at scale. It connects banks, merchants, and payment apps on one simple network. Users can pay instantly, anytime, without needing a credit or debit card.

Open banking isn’t limited to banks. Many non-financial companies are using APIs to bring financial tools directly into their platforms.

A retailer can now offer banking features right inside its app. Customers can check balances, track spending, or move money using the same interface they shop from.

Businesses need to plan their API strategy carefully. Strong partnerships and smart data sharing will drive agility, innovation, and a better customer experience in the years ahead.

Digital currencies are shaping the next big wave of fintech trends. They include central bank digital currencies (CBDC) and cryptocurrencies. Both are changing how people and businesses move money.

Major economies are testing national digital currencies. These trials aim to make cross-border payments faster, cheaper, and more transparent. At the same time, private crypto projects are working on stability and regulatory compliance, trying to build trust with both investors and governments.

Tech-savvy financial professionals are also stepping in here. They’re developing safer systems, improving transparency, and helping organizations understand how to operate confidently within the digital currency world.

Some central banks are already piloting digital currencies backed by a digital ledger. The goal is simple: reduce costs, increase transparency, and cut the middle steps that slow international transfers.

Investors can now buy cryptocurrency ETFs, tokenized funds, and digital assets without handling crypto directly. These products open the door to new markets and make digital finance easier to access.

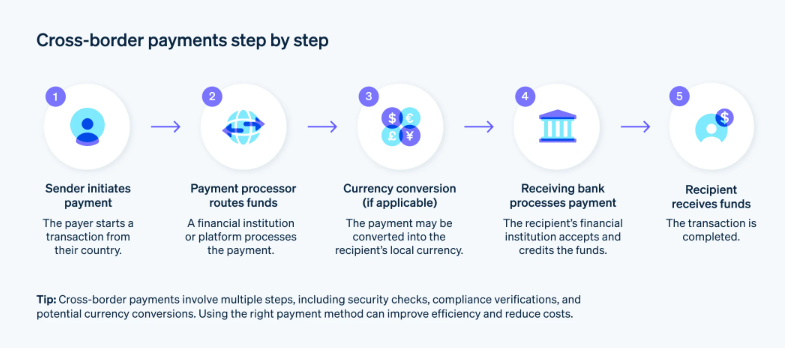

Glocal payments, which are global payments with a local touch, are another important fintech trend for 2026. People expect to send, receive, and manage money across borders as easily as they do at home. Businesses want the same simplicity when paying suppliers or collecting payments from customers.

Modern payment technologies now make that possible. Transfers that once took days now happen in seconds. A worker living abroad can use a mobile wallet to send money home in real time. The families receive funds instantly with low fees, thanks to new digital payment systems.

A global supplier can also track shipments, offer financing, and receive payments instantly through one fintech platform. Smart systems handle the paperwork, reduce errors, and keep transactions transparent.

For any business expanding across borders, the goal is clear: think local but act global. Payment rules, customer habits, and regulations differ by market. Understanding those differences is what turns financial technology into a true growth tool.

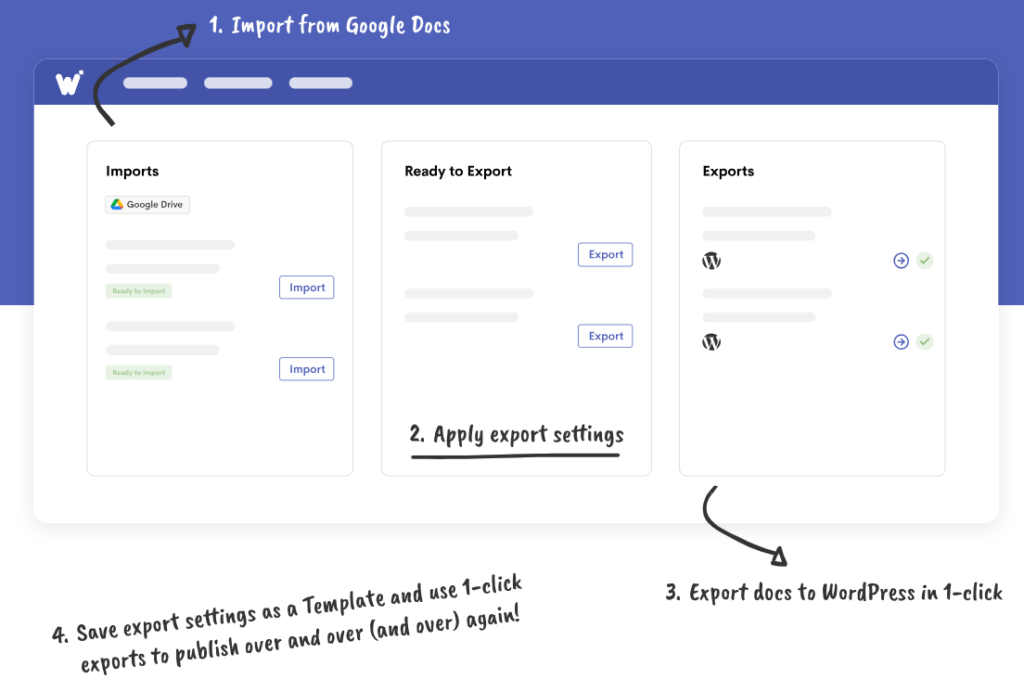

The fintech world is moving fast, and so is the way companies share what they learn. Today, content isn’t just about writing blog posts. It involves turning complex ideas into stories that people can understand and act on. And that’s where tools like Wordable make a difference.

Fintech teams now use data analytics in content marketing to learn what really connects with readers. They track engagement data, topic performance, and audience behaviour to shape better messages and publish faster. By turning numbers into insights, they make sure every article, report, or update drives real results.

With Wordable, this process gets easier. Teams can skip the time-consuming formatting and uploading steps, as the process lets them publish their Google Docs to WordPress in one click. It also works for HubSpot and Medium users.

Then, they can focus on creating engaging content that reflects their fintech expertise. That way, they share valuable insights at the right time, reaching the right audience when it matters most.

The pace of change in finance isn’t slowing down. And that’s good news for innovators. The fintech trends we’ve just discussed show a clear direction: smarter data, faster payments, and more accessible financial tools for everyone.

Whether you’re leading a fintech startup, managing content for a financial brand, or simply curious about the next wave of technology, the key is to stay informed and act fast.

With Wordable, you can do just that. It helps your team publish research, insights, and long-form content in minutes instead of hours, so your fintech stories reach your audience while the topic is still hot.

Try Wordable and start turning your fintech expertise into content that performs.

In 2026, artificial intelligence, blockchain, embedded finance, open banking, and digital currencies are leading the way. These technologies make finance faster, safer, and more personal.

AI improves fraud detection, customer service, and data analysis. Banks and fintech companies use AI to predict spending habits, detect unusual activity, and offer tailored recommendations.

Yes, but their role is shifting. Traditional banks are forming partnerships with fintechs, adopting open banking systems, and upgrading infrastructure. The institutions that adapt will stay ahead.

Security is improving, but it still matters where you choose to bank or invest. Look for platforms with strong authentication, clear regulatory transparency, and trusted partners. Being cautious helps you benefit safely.

Fintech brands can use content planning tools to publish faster and maintain accuracy. Platforms like Wordable help teams save time by automating formatting and uploads, turning insights into ready-to-publish content.